Published by Tapton Capital

2026

Notice Accounts: Maximise Savings with Flexible Access

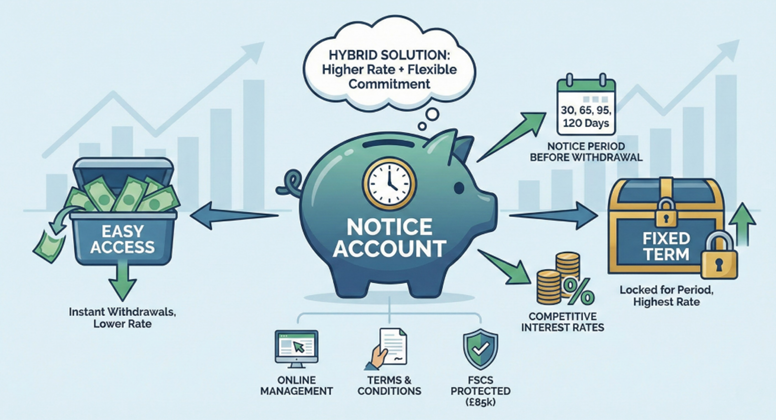

In today's financial landscape, finding the right savings account can be a crucial step towards achieving your financial goals. Among the various options available, the notice account stands out as a hybrid solution, blending the benefits of both easy access and fixed-term accounts. A notice account allows you to earn a higher interest rate than a standard easy access savings account while still providing access to your funds. This is achieved by requiring you to give a notice period before withdrawal.

What is a Notice Account?

A notice account is a type of savings account that offers a higher interest rate in exchange for you agreeing to a notice period before you withdraw funds. This notice period before withdrawal can be anywhere from a few days to several months, depending on the specific terms of the account. Think of it as a middle ground between an easy access account, which allows instant withdrawals but typically offers lower interest rates, and a fixed-term bond, which locks your money away for a set period but usually provides the highest returns. What is a notice account's core function? It helps you earn more without completely restricting access to your funds.

Key Benefits of Notice Accounts

- Higher interest rates than easy access accounts

- Flexible access to funds with advance notice

- Better returns than standard savings accounts

- Ideal for strategic liquidity management

- No complete lock-in period like fixed-term bonds

For example, consider someone saving for a down payment on a house. They might want to keep their money relatively accessible in case they find the perfect property sooner than expected. A notice account with a 30-day notice account requirement could be ideal. It offers a better interest rate than an easy access account while still allowing them access to their savings within a reasonable timeframe. This blend of balance, accessibility and growth makes a notice account a powerful tool for strategic liquidity management.

Features and Benefits

Notice accounts come with a range of features and benefits that make them an attractive option for savers who want to earn competitive interest rates without sacrificing all access to their money. Understanding these features is key to determining if an account aligns with your financial goals.

Features of the Set Notice Deposit account

Let's delve into some common characteristics you'll find in a typical notice deposit.

Core Features

- Higher Interest Rates: Notice accounts generally offer a higher interest rate than easy access savings accounts. This is the primary incentive for accepting the withdrawal notice requirement.

- Notice Period: This is the defining feature. You must give a notice period, ranging from 35 days, 65 days, 95 days, or even 120 days, before a withdrawal can be made. The length of the notice period impacts the rate offered.

- Variable or Fixed-Rate Savings Accounts: Some notice accounts offer a variable interest rate, which means the rate can fluctuate with market conditions. Others offer a fixed interest rate for a specified period, providing more certainty.

- Minimum Deposit Requirements: Most notice accounts have a minimum deposit required to open a notice account today. This amount can vary significantly between financial institutions.

- Limited Withdrawals: While you can withdraw funds, doing so requires adhering to the notice period. Failing to give a notice period before you withdraw funds might result in a penalty fee or loss of interest.

- Online Management: Many notice accounts are managed online, providing convenient access to your account and allowing you to track your savings.

The core advantage of a notice account lies in its ability to unlock higher interest tiers while offering a degree of flexible commitment. By accepting the notice period, you demonstrate a commitment to saving, which the financial institution rewards with a more competitive interest rate. This structured savings approach can be particularly beneficial for cultivating disciplined saving habits.

Rates

Interest rates on notice accounts are constantly in flux, influenced by factors such as the overall economic climate and the policies of individual banks. However, as a general rule, the longer the notice period, the higher the interest rates you can expect to receive. It's important to shop around and compare notice accounts from different providers to find the most competitive rates.

Understanding Notice Account Rates

For example, GB Bank's Capital Growth Account might offer a rate, with a higher rate for accounts requiring 95 days' notice compared to those requiring only 35 days' notice. Similarly, Bank of Ireland's 31-day set notice account offers a specific interest rate on deposits, contingent on the 31-day notice period being observed. These examples highlight the direct correlation between the notice period and the potential return on your investment.

Keep an eye on sites that provide competitive analysis of savings products. These resources can help you identify institutions offering the best notice account rates at any given time. Remember, even a small difference in the interest rate can make a significant impact on your savings over the long term. Make sure to factor in the Annual Equivalent Rate (AER) to understand the true annual return.

How Notice Accounts Compare to Other Savings Options

To fully appreciate the value of a notice account, it's crucial to understand how it stacks up against other common savings accounts. Each option has its own set of advantages and disadvantages, making it suitable for different financial goals and circumstances.

Fixed Rate Accounts

Fixed-term accounts, also known as fixed-rate bonds, offer a guaranteed interest rate for a specified period, typically ranging from one to five years. While they often provide the highest interest rates available, they also come with strict conditions. Withdrawals require a significant penalty or are simply not allowed until the maturity dates.

When to Choose Fixed-Term Accounts

Fixed-term accounts are best suited for individuals who have a clear savings goal with a defined timeline and are confident they won't need access to their funds during the term. For example, if you're saving for a wedding that's three years away, a three-year fixed-rate bond could be a good option. However, if you anticipate needing your money sooner, a notice account might be a better choice.

Easy Access Accounts

Easy access accounts offer the ultimate flexibility, allowing you to withdraw funds at any time without restrictions. However, this convenience comes at a cost: easy access savings accounts typically offer the lowest rates.

When to Choose Easy Access Accounts

These accounts are ideal for building an emergency fund or for individuals who need frequent access to their savings. For example, if you want to maintain a financial buffer for unexpected expenses, an easy access account is a sensible choice. However, if you're looking to maximise your returns and don't need immediate access to your money, a notice account can provide a significant boost to your savings.

Fixed Rate Cash ISA

Fixed Rate Cash ISA is a tax-efficient savings account that offers a fixed interest rate for a specified period, similar to a bond. The key difference is that any interest earned within an ISA is tax-free, up to the annual ISA allowance. The current ISA allowance is £20,000 for the 2024/2025 tax year.

If you haven't already used your ISA allowance, a fixed-rate cash ISA can be an excellent way to save tax-free. However, like fixed-rate bonds, they typically have limited access conditions, with withdrawals requiring a penalty.

Opening and Managing Your Notice Account

Opening a notice account is a straightforward process, but it's essential to understand the steps involved and the information you'll need to provide. Financial resilience is achieved through informed decisions, so let's walk through the process.

How to Apply

The application process for a notice account is generally similar across different financial institutions. You'll typically need to provide the following:

1

Personal Information

This includes your name, address, date of birth, and contact details.

2

Identification

You'll need to provide proof of identity, such as a passport or driver's licence.

3

Proof of Address

A recent utility bill or bank statement can serve as proof of address.

4

Tax Information

You may need to provide your tax identification number (e.g., National Insurance number in the UK).

5

Funding Source

The bank will need to know where the funds you're depositing are coming from to comply with AML (Anti-Money Laundering) regulations.

The application can usually be completed online or in person at a branch. Customer onboarding is made easier with online banking platforms.

Book an Appointment

Some banks, like Bank of Ireland, offer the option to book an appointment with a financial advisor to discuss your savings needs and help you choose the right notice account. This can be particularly helpful if you're unsure which account is best suited for your financial goals.

Funding Your Notice Account

Once your notice account is open, you'll need to deposit funds to start earning interest. Most accounts have a minimum deposit amount, which can range from a few hundred pounds to several thousand. What is the maximum balance on notice accounts? It varies, so check the specific terms.

How do I make additional deposits into my notice account?

Most financial institutions offer several convenient ways to deposit funds into an account.

Deposit Methods

- Electronic bank transfers: This is the most common method. You can transfer funds from another bank account to your notice account using online banking or a mobile banking app. You'll need the account number and sort code for your notice account.

- Cheque: You can also deposit funds by mailing a cheque to the bank. Make sure to write your notice account number on the back of the cheque.

Accessing Your Funds: The Notice Period

The defining characteristic of a notice account is the notice period. This is the amount of time you must give as a notice period before you can withdraw funds. The length of the notice period can vary, but it's typically 35 days, 65 days, 95 days, or 120 days.

To withdraw funds, you'll need to notify the bank of your intention to make a full withdrawal or partial withdrawals. This can usually be done online, by phone, or in writing. Once the notice period has expired, you'll be able to access your funds.

Important information on using Notice to make withdrawals from your account

It is essential to carefully read the Terms and Conditions before you open a notice account. Here's some key information to keep in mind:

- Starting the Notice Period: Understand how the notice period is triggered. Does it start the day you submit your withdrawal request or the next business day?

- Withdrawal Options: Clarify whether you can make partial withdrawals or only full withdrawals.

- Penalty for Withdrawal: Be aware of any penalty for withdrawal that may apply if you withdraw funds before the notice period has expired. The penalty fee might involve losing a portion of the interest you've earned.

- Minimum Withdrawal Amount: Check if there's a minimum withdrawal amount.

Understanding these details will help you avoid any surprises when you need access to your funds.

Managing Your Account

Managing your notice account is generally a simple process, especially with the prevalence of online banking. You can typically view your balance, track your interest earnings, and submit withdrawal requests through the bank's website or mobile app. These also provide a savings calculator.

How do I cancel my scheduled transactions?

If you have scheduled a withdrawal and need to cancel it, you should contact the bank as soon as possible. The process for cancelling a scheduled transaction may vary depending on the bank, so it's best to check their FAQs or contact customer support.

Understanding Interest and Taxes

Interest earned on notice accounts is typically subject to tax. However, the amount of tax you pay will depend on your individual circumstances and the applicable tax laws. Understanding DIRT is crucial.

What if my rate changes?

If you have a variable-rate notice account, the rate can change over time, reflecting changes in the market. The bank will typically notify you in advance of any rate changes. If the rate goes down, you may want to consider switching to a different account with a higher rate.

What is the Personal Savings Allowance?

The Personal Savings Allowance (PSA) is a UK tax allowance that allows individuals to earn a certain amount of interest on their savings tax-free. The amount of the PSA depends on your income tax band. For basic rate taxpayers, the PSA is £1,000. For higher-rate taxpayers, it's £500. Additional rate taxpayers do not receive a PSA.

Account Limits and Security

Notice accounts may have certain limits on the amount you can deposit or withdraw funds. These limits are typically outlined in the account Terms and Conditions.

Banks employ robust digital security measures, including data encryption and two-factor authentication, to protect your account from fraud and unauthorised access. KYC (Know Your Customer) and AML (Anti-Money Laundering) are also important compliance measures.

What is the maximum balance on notice accounts?

The maximum balance on notice accounts will vary depending on the financial institution offering the account. Some may have no limit, while others may impose a cap. It's important to check the specific terms of the account before you open a notice account.

Deposit Guarantee Scheme

Your eligible deposits in notice accounts are protected by the Financial Services Compensation Scheme (FSCS). The FSCS Protection Scheme protects up to £85,000 per eligible depositor per financial institution. This means that if the bank were to fail, you would be compensated up to this amount. This is similar to the Deposit Insurance Corporation (FDIC) in the United States.

FSCS Protection Details

Background

The FSCS is the UK's statutory deposit insurance scheme. It was established to protect depositors in the event of a bank failure.

Eligible Deposits

Most deposits held with Financial Conduct Authority (FCA) authorised banks, building societies, and credit unions are eligible for FSCS protection. This includes notice accounts, easy access accounts, and fixed-term bonds.

Protected Depositors

The Deposit Insurance Scheme protects individuals, small businesses, and charities.

General limit of protection

The general limit of protection is £85,000 per eligible depositor per financial institution.

Temporary high balances

Temporary high balances, such as those resulting from the sale of a property, may be protected for up to £1 million for a period of six months.

Limit of protection for joint accounts

For joint accounts, each depositor is protected up to £85,000, meaning a joint account with two depositors would be protected up to £170,000.

Compensation Payment Procedure

If a bank fails, the FSCS will aim to pay compensation within seven days. This can be done via electronic bank transfers.

Terms and Conditions

Before opening a notice account, it's essential to carefully read and understand the terms and conditions. These documents outline the access conditions, interest rate terms, withdrawal procedures, and any fees or charges that may apply. Regulatory compliance is paramount for banks.

To find out more about the product, download our information sheet. Many banks provide detailed information sheets about their notice accounts. These sheets typically provide a summary of the key features and benefits of the account.

Customer Support and Resources

Customer support is a vital aspect of any financial institution. Banks typically offer a range of customer support channels, including online chat, phone support, and email support. They also provide resources such as FAQs and educational materials to help you understand their products and services. Financial literacy is important.

Available Support Resources

- Online chat support

- Phone support

- Email support

- FAQs and educational materials

- Customer reviews and testimonials

- Quick links to important information

Conclusion

Maximising Your Savings with Notice Accounts

In conclusion, the notice account provides a compelling option for savers seeking a balance between access and growth. By understanding the features, benefits, and access conditions of notice accounts, you can make an informed decision that aligns with your financial goals. Remember to carefully consider your liquidity needs and shop around for the most competitive interest rates to maximise returns with notice.

Notice accounts offer a strategic middle ground for savers who want to earn competitive interest rates without completely locking away their funds. Whether you're saving for a house deposit, planning for future expenses, or building your savings portfolio, a notice account can be an excellent tool for achieving your financial objectives while maintaining flexibility.

FAQs

What is the difference between a notice account and a fixed-term deposit?

A notice account requires you to give a notice period before you can withdraw funds, while a fixed-term deposit locks your money away for a set period. Notice accounts typically offer more flexibility than fixed-term accounts.

Is a notice account right for me?

A notice account is a good option if you want to earn a higher interest rate than an easy access account but still need some degree of access to your funds.

What happens if I need to withdraw funds before the notice period?

You may be subject to a penalty for withdrawal, such as losing a portion of the interest you've earned.

How do I choose the best notice account?

Compare interest rates, notice periods, minimum deposit requirements, and any fees or charges before opening a notice account. Also, check the provider's reputation.

Are notice accounts safe?

Yes, eligible deposits in notice accounts are protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per eligible depositor per financial institution.

Can I top up my notice account?

Most notice accounts allow you to top up the balance at any time. However, it is best to check the specific terms and conditions of the account.

What are the pros and cons of a notice account?

The pros include higher interest rates and some access to your funds. The cons include the notice period requirement and potential penalties for early withdrawal.

How does a notice account benefit business cash flow?

A notice account can help businesses optimise their business cash flow by earning competitive interest rates on short-to-medium-term savings while maintaining some access to their funds.

Where can I find the best notice account rates?

You can find the best notice account rates by comparing accounts from different financial institutions online. Look for comparison websites that provide competitive analysis.

What should I consider before opening a notice account?

Before opening a notice account, you should consider your financial goals, liquidity needs, and risk tolerance. You should also carefully review the Terms and Conditions of the account.

Are there any account-keeping fees associated with notice accounts?

Some financial institutions may charge account-keeping fees for notice accounts. It is important to check the fee structure before opening a notice account.

What are the tax implications of a notice account?

Interest earned on notice accounts is typically subject to tax. However, you may be able to use your Personal Savings Allowance to earn some interest tax-free.

How do I give advance notice to withdraw funds?

You can typically give a notice period to withdraw funds online, by phone, or in writing, depending on the financial institution's procedures.

What is the Yield-Optimised Access Account?

A yield-optimised access account is a type of notice account that aims to provide the best possible interest rate while still allowing some access to your funds.

By understanding the nuances of notice accounts, you can strategically use them to enhance your financial resilience and work towards capital growth.

Need Help with Notice Accounts?

If you're looking to maximise your savings with a notice account, Tapton Capital can help. Our specialist team provides expert advice on savings products, helping you understand your options, compare rates, and choose the right account for your financial goals. Contact us today for a free consultation.

Get Free Consultation

Call Now